Financial Times: "No one needs to buy Tesla"

(29 March 2018)

After the recent crash in Tesla's stock and bonds prices, it seems like a good time to revisit an idea that has long underpinned the value of the shares: the string of companies supposedly dying to buy the car and battery maker should the opportunity arise.

As we wrote three years ago, when Elon Musk was a superstar and people thought it was reasonable for Apple to pay $75bn to hire him, no-one needs to buy Tesla.

Since then the price tag has doubled, from about $25bn to $51bn, including debt. But that simply reinforces our previous argument: it would be much cheaper to build Tesla from scratch.

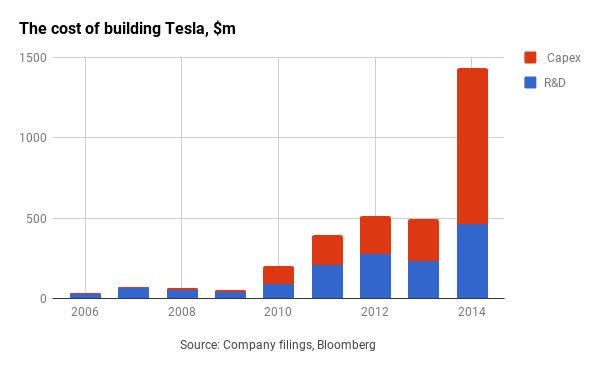

In early 2015, we calculated that Tesla had invested $3.1bn in capital spending and research and development up to that point:

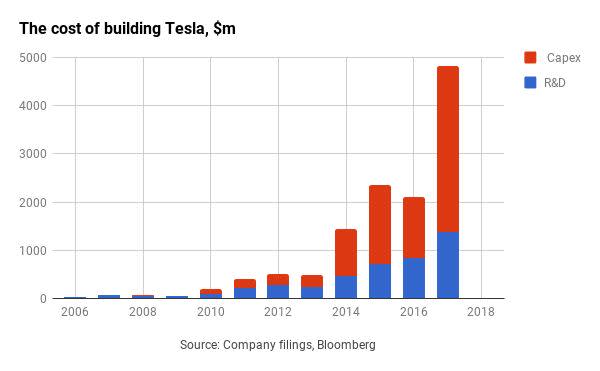

Mr Musk, helped by the bond market and his bankers, who facilitated margin loans so he could buy stock in Tesla's equity raises, has since thrown much more money at the business:

The R&D and capex spend to date is about $12.5bn, with perhaps an additional $5bn earmarked for this year, totalling $17bn. For anyone willing to pay three times that amount today, the company comes with all its engineers, and of course the mercurial Mr Musk.

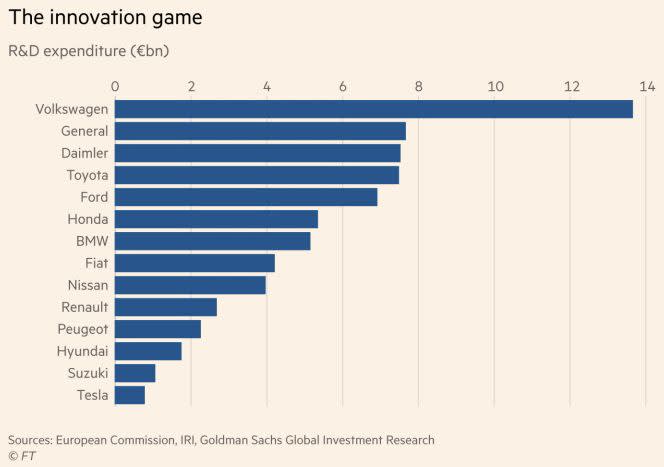

Carmarkers have not been standing still, however. Volkswagen is forecast to drop €53bn ($66bn) on capital expenditures over the next three years, and has a range of high-performance electric cars coming down the track.

VW's is the biggest investment programme in the industry, but take a look at the chart from a recent FT Big Read on the industry's electric car plans:

Clearly, not all of the money above goes toward electric car development, but whatever lead Tesla has over the rest of the industry is rapidly shrinking. With its lead goes the illusion that it makes sense for a competitor to catch up by buying a company for four or five times the value of its relevant assets (property, plant and equipment, and intangible assets are under $11bn).

Note too that Tesla's recent investments in technology might not have been cost effective. A report from Max Warburton of Bernstein Research on Wednesday argued that Tesla's attempts to automate final assembly for its mass-market Model 3 may be behind the well-documented production problems.

Claiming experience at MIT, where he benchmarked assembly plants, Max says Tesla “appears to be ignoring automotive history”:

Few have seen it (the plant is off-limits at present), but we know this: Tesla has spent c.2x what a traditional [original equipment manufacturer] spends per unit on capacity. It has ordered huge numbers of Kuka robots. It has not only automated stamping, paint and welding (as most other OEMs do) - it has also tried to automate final assembly (putting parts into the car). It talks of two-level final lines with robots automating parts sequencing. This is where Tesla seems to be facing problems (as well as in welding & battery pack assembly).

Tesla would no doubt point to its ambitions to shake up the industry again and do things differently, with lots of robots. It has come this far, after all. Max has doubts:

What is the inspiration behind Tesla's automation? Tesla has bought German robots and a German automation company (Grohmann). But the German OEMs – traditionally the most enthusiastic proponents of automation – have actually been rowing back on it in recent years. The best producers - still the Japanese - try to limit automation. It is expensive and is statistically inversely correlated to quality. One tenet of lean production is “stabilise the process, and only then automate”. If you automate first, you get automated errors. We believe Tesla may be learning this to its cost.

Tesla has got to where it is, carrying $10bn of debt to fund its ambition to do things differently, because the nature of its challenge is quite unlike most large listed companies. Willing customers aren't the problem. It is producing a product -- a $35,000 electric car -- that people have already lined up to buy if it can. Tesla is, effectively, the world's largest-ever GoFundMe campaign.

So what about the brand?

Imagine the worst case, where it doesn't work out this year. Tesla's production line requires rebuilding or rejigging substantially to churn out cars in very large numbers.

Perhaps it would make sense for another carmaker to step in, with expertise and deep pockets, for a big potential share of the future electric car market.

Ignore the loss-making battery and solar bits of Tesla. Last year it sold 103,000 expensive cars, for $9.6bn. That is pretty similar to Porsche in 2007, which sold 98,000 cars for $9.7bn (€7.4bn).

At the time, near the top of the market boom as it began to get entagled with VW, Porsche was valued at around $36bn including debt, according to Bloomberg. It had less world-changing potential, perhaps, but it was also reliably profitable [e.g. highest margins in the sector] and not swallowing cash.

Maybe Tesla's brand could be worth half as much again, and maybe its production lines need mere tweaks to sort out delays. If the latter doesn't work out, however, the former looks like the wrong assumption on which to rest a valuation.

FT Link: http://ftalphaville.ft.com/2018/03/28/1522248619000/No-one-needs-to-buy-Tesla/